(Zerohedge) – Banks are enormously complex beasts. They are not simple businesses. To turn around a bank is complex. To reinvent a bank – which is what Deutsche Bank, UBS, CS, and others are desperately trying to do, is one level below impossible.

Earlier this year, we had commodities firm Glencore teeter on the edge of disaster. Swift action, clear plan, and it’s back from the brink. That is not going to happen with banks. In my 30 years of markets, I can’t think of a single bank that’s got in trouble that has staged anything like a similar comeback. Once banks catch a cold, it often develops into dangerous pneumonia.

Deutsche – and the others – are anything but healthy. They need to reinvent. The news flow yesterday was positive-ish. Rumors of a SWF capital injection, rumours of a domestic rescue plan, but the reality is more likely to be further deterioration. If that develops into a full crisis any rescue will come at the cost of contingent capital deals being triggered (which will send shock-waves around banking confidence) and the strong/inevitable bail-in of senior debt holders.

The U.S. Department of Justice fine imposed on Deutsche Bank is very high and “damaging for financial stability,” Dutch Finance Minister Jeroen Dijsselbloem tells lawmakers in The Hague Thursday.

U.S. fines against European banks are “repeatedly so high that all the money European banks tap on the international markets, also from U.S. investors, is skimmed by the U.S. government. That’s a risk for the financial stability and that worries me sincerely.” If Deutsche Bank has to pay the $14b fine, it will reduce capital, then it will have to raise new capital. Deutsche Bank will have to bring things “back in order.”

~~~~~

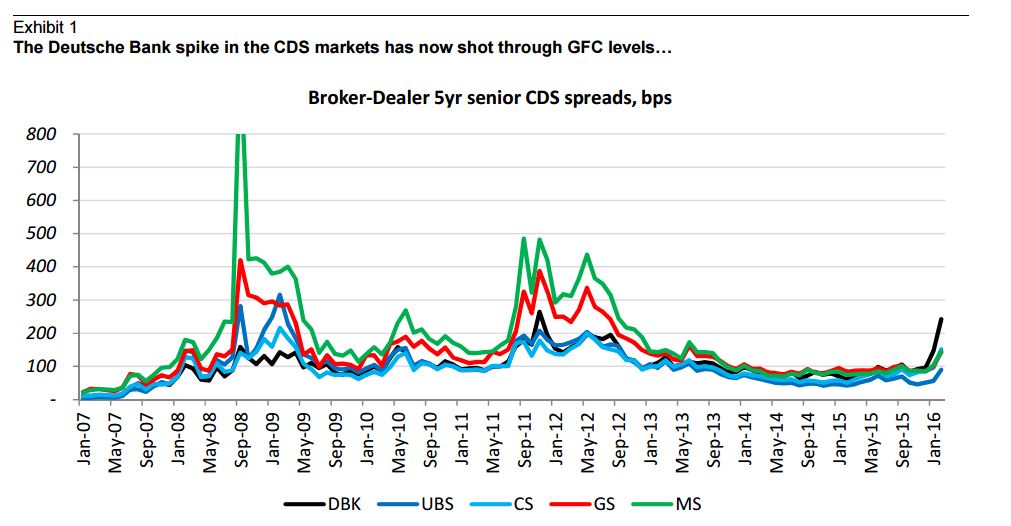

As the above chart shows, the cost of short-term Credit Default Swaps for Deutsche Bank has again gone through the roof, but that is only part of the picture. Since December 2015, the cost of longer term (5 Year) CDS for DB has been climbing well above its peers, as shown here –

As the chart clearly depicts, DB (the black line) had been right in among its peers, but starting in the last weeks of calendar year 2015, it has risen out of the pack, and by the end of January 2016 was drawing a premium twice that of Morgan Stanley, and just shy of 3 times that of UBS.

And, as shown below, the total risk to the Euro-denominated market has now coupled with the CDS-fault risk of DB. Or in other words, the risk to the entire Euro market is now dominated by the risk of just one bank – Deutsche Bank.

This is what “INEVITABILITY” looks like. Deutsche is now demonstrably past the point of recovery, and it is only a matter of time before DB comes crashing down under the weight of its own dangerous and failing “investment strategy.”

The executives of Deutsche Bank lied and cheated their way through the 2008-09 financial crisis, and thus avoided facing the music along with everyone else at that point in time. What that bought them was time and opportunity, which their management used, not to save the bank by quietly winding down their failing positions, but rather to double down on their already-failing investments in bubble-priced real-estate, and the issuance of even more toxic derivatives.

WE HAVE BEEN WARNED